Key Takeaways

-

Balance transfers offer relief from high-interest payments, granting individuals more time to navigate and alleviate their debts.

-

A zero-percent balance transfer allows moving debt to a card with a promotional period where no interest is charged, saving significant money on interest.

-

While introductory rates may be as low as 0%, balance transfer fees typically range from 3-5% of the transferred amount.

In times of financial crisis, survival often hinges on borrowing, leading to mounting debt.

Proactive financial planning becomes pivotal in such situations, and for those with credit scores still intact, a potential lifeline of balance transfers emerges!

Thus, understanding what is a balance transfer is crucial for effective debt management.

This financial maneuver involves moving existing debt from one credit card to another, often at a lower interest rate, offering a strategic approach to ease financial burdens.

In this comprehensive guide, we’ll delve into balance transfers, exploring the process, benefits, types, and best practices to make the most of this financial tool.

What is a Balance Transfer?

A balance transfer is a strategic financial move where outstanding debt from one credit card is transferred to another.

It is often done to take advantage of lower interest rates offered by the new card to avoid accumulating interest on the existing debt.

A subset of this is the 0% balance transfer, a popular choice for those seeking relief from high-interest debt.

This maneuver can streamline debt management and potentially save the individual’s money on interest payments.

How do balance transfers work?

A balance transfer process involves a credit card issuer paying off your existing debt with another lender, and you then owe the new card issuer.

In simple words, the new credit card pays off the existing debt on the old card, essentially transferring the owed amount to the new card.

This process is typically employed to benefit from a lower interest rate with a low or 0% introductory APR on the new card, allowing individuals to repay their debt more efficiently.

While balance transfers usually incur a fee, it becomes cost-effective if the fee is less than the interest accrued on the existing account.

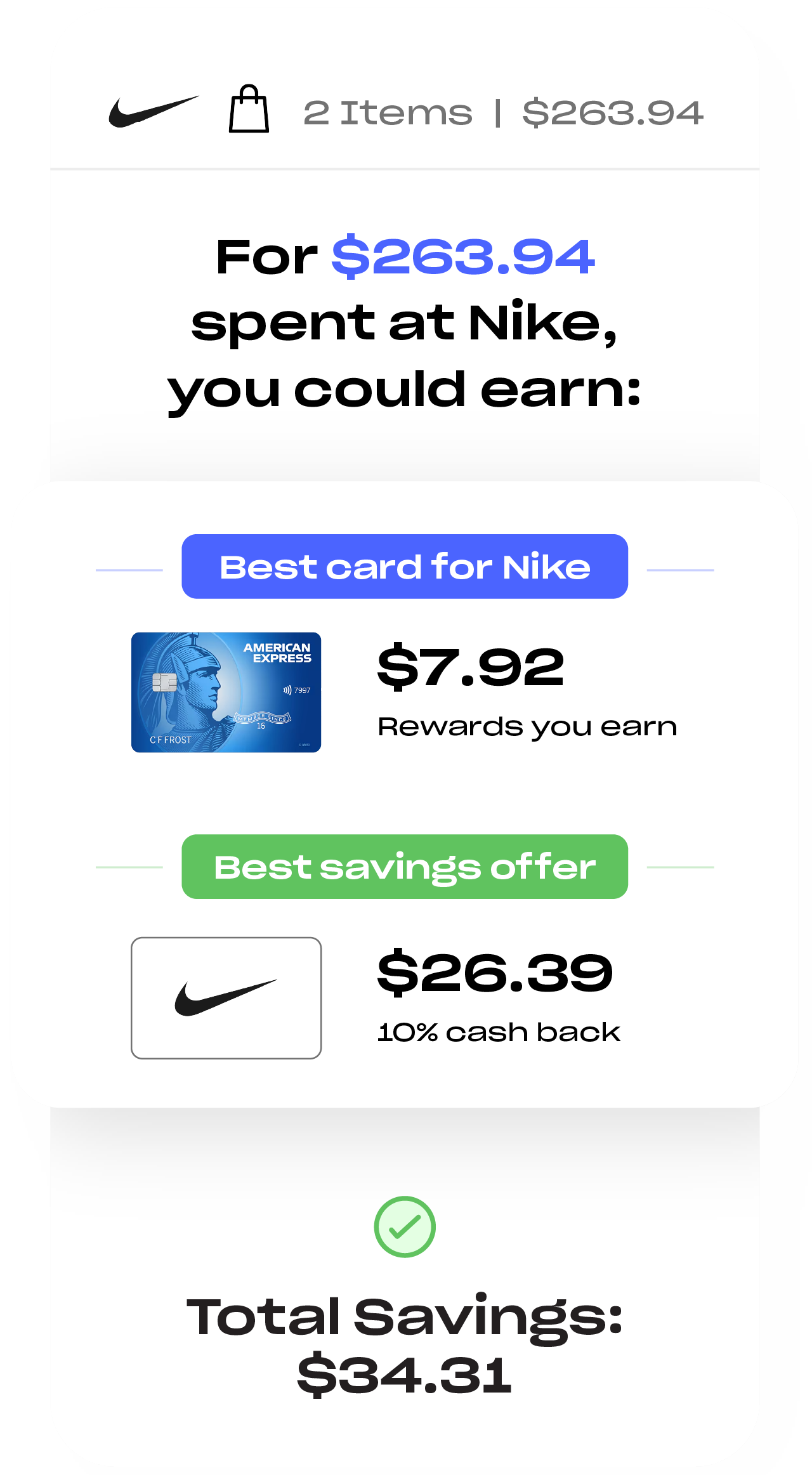

For Example– Transferring a $10,000 balance from a high-APR credit card A to a low-APR credit card B can save you money.

Assuming the card B’s credit limit allows, they pay $10,000 to card A, and then you owe card B $10,000.

Despite a potential balance transfer fee, if the new card has a 0% introductory APR for 15 months and you repay within this period, you could save approximately $1,096 compared to the original 20% APR card.

It offers significant interest savings and is an effective way to manage credit card debt efficiently.

How to do a balance transfer?

Initiating a balance transfer is a straightforward process that can significantly impact your financial well-being.

Follow these steps to navigate the process seamlessly and make the most of this debt management tool.

-

Evaluate your Debt Situation

Evaluate your Debt SituationAssess current debts, balances, interest rates, and terms.

Then, identify suitable debts for transfer, forming the basis of an effective debt management plan.

-

Check your Credit Score

Check your Credit ScoreKnow your credit score to boost eligibility for favorable balance transfer offers.

A higher credit score increases the likelihood of securing lower interest rates and better terms.

-

Research and Apply for Ideal Offer

Research and Apply for Ideal OfferExplore various issuers for attractive balance transfer offers, prioritizing low or 0% introductory APR, extended promotional periods, and minimal fees.

Apply for the chosen card with a suitable credit limit.

-

Initiate and Monitor Transfer Process

Initiate and Monitor Transfer ProcessUpon approval, contact the credit card issuer to initiate the balance transfer, adhering to set limits.

Monitor the process closely and create a strategic repayment plan with transferred balances, utilizing the 0% APR period effectively and avoiding new purchases on the transfer card.

Whether you’re eyeing a Chase balance transfer or exploring the options with American Express, understanding the unique procedures of different credit card issuers is crucial. Take charge of your financial journey with confidence!

-

How to do a Balance Transfer with American Express

To initiate a balance transfer with American Express, note that you can only do that from another issuer’s card to an Amex card, not between Amex cards.

Compare Amex balance transfer cards, considering intro APR periods, rewards, and fees. The balance transfer fee is typically 3% (minimum $5), and the standard variable APR applies after the intro period.

For new Amex card applications, enter the necessary information during the process.

If you have an existing eligible Amex card within the intro APR period:

- Log in to your account

- Navigate to “Account Services”

- Choose “Payment & Credit Options”

- Click “Transfer Balances” and provide the required details.

- Alternatively, call Amex customer service for assistance.

-

How to do a Balance Transfer with Citi

Citi provides extensive balance transfer options with up to 21 months of introductory APR, a significant window to manage high-interest debt.

To initiate a balance transfer with a new Citi card, apply for a card, get approved, and transfer the balance during the application process.

Transfer within four months of account opening for existing Citi cards like Citi Simplicity, Citi Diamond Preferred, Citi Double Cash, and Citi Rewards+.

Log in to your Citi account, go to Payments and Transfers, choose “Balance Transfers,” and select the offer.

Enter details like the account number and transfer amount.

Beyond the four-month limit, you may still receive offers periodically.

Contact Citi customer service for assistance!

-

How to do a Balance Transfer with Wells Fargo

To perform a Wells Fargo balance transfer, get approval for the new card, and choose one of three methods: online through your Wells Fargo account, over the phone (1-800-642-4720), or by using balance transfer checks.

Provide your existing credit card details and the total balance to transfer.

For online transfers, log in, select Account Management, and then “Request Balance Transfer.”

Approval depends on creditworthiness, requiring a good to excellent credit score and a debt-to-income ratio below 36%.

Utilize the introductory APR by completing the transfer within 120 days, with varying balance transfer fees depending on the Wells Fargo card.

-

How to do a Balance Transfer with Bank of America

To transfer a balance to a Bank of America credit card, you must complete the process within the first 60 days of account opening.

The transfer incurs a 3% balance transfer fee, and exceeding the credit limit may result in a partial transfer or denial.

Pay off balances before the introductory APR period ends to avoid regular variable APR charges.

Online balance transfers for new and existing cards involve completing an application, requesting a transfer, and providing the necessary details.

Most transfers take two to four days, with new accounts possibly requiring up to 14 days for completion.

-

How to do a Balance Transfer with Chase

Before making a balance transfer with Chase, keep in mind that transferring debt between two Chase cards is not allowed.

There’s typically a 3% intro balance transfer fee (minimum $5) on most Chase cards, factored into your total balance.

You can leverage a 0% intro fee by transferring the balance within 60 days of account opening.

Ensure the transferred amount doesn’t exceed your credit limit.

To transfer a balance to a new Chase card, apply, get approved, and then request the transfer online by providing the necessary details.

For an existing Chase card, log in, check for balance transfer offers, and follow the prompts to complete the transfer.

You can also call customer service for assistance.

-

How to do a Balance Transfer with Capital One

To start a Capital One balance transfer, choose between using an existing credit card or obtaining a new one.

You can’t transfer balances between two Capital One cards. Only balances from external issuers, like Discover or Citi, can be transferred.

The transfer may be restricted, if your total, including fees, surpasses your credit limit.

For an existing card, log in to your Capital One account, select the credit card, and navigate to “Transfer a balance.” Enter details of the other issuer, ensuring the transfer aligns with the offer.

With a new card, perform the transfer during the application process after approval.

Capital One indicates immediate processing upon approval, taking approximately 10 business days with the other issuer.

What happens after you transfer a balance?

Once you’ve initiated a balance transfer to a credit card, you must ensure timely payment of at least the minimum amount specified by the card issuer each month, as indicated on your monthly bill.

This practice is crucial for maintaining a positive account status and preserving any 0% introductory APR your card might provide.

However, it’s important to note that, eventually, you’ll have to increase the monthly minimum payment.

Additionally, individuals should be mindful of any fees associated with the transfer and be aware of the interest rate that will apply after the promotional period ends.

Cards featuring a low introductory balance transfer rate usually transition to a higher regular APR, which applies to any remaining balance once the intro period ends.

What is a 0% Balance Transfer?

A zero-percent balance transfer involves moving debt to a new credit card with a promotional period during which no interest is charged.

This provides individuals with a much-needed window of time to pay off their debt without incurring additional costs from interest charges.

The 0% APR is a key feature that attracts individuals looking to save money on interest payments and expedite their journey to debt freedom.

However, consumers need to recognize that the interest-free period is limited, and after this introductory phase, a standard APR will apply.

A 0% interest, balance transfer credit card offers a valuable opportunity for individuals looking to manage existing debts more efficiently.

Credit card companies profit from interest and merchant swipe fees, emphasizing the importance of understanding the terms and ensuring that the benefits align with individual financial goals.

Balance Transfer Rates and Fees

While the introductory rate for a balance transfer is often 0%, some credit cards may charge a balance transfer fee, typically ranging from 3-5% of the transferred amount.

It’s important to factor in these fees when considering a balance transfer for accurately assessing the overall cost-effectiveness.

For example, a $100 balance transfer incurring a 5% fee would result in a new balance of $105.

It’s essential to carefully calculate these fees against the potential costs of carrying a balance until it’s paid off.

Sometimes, the fees associated with balance transfers might outweigh the expense of maintaining a balance, especially for short-term balances.

Careful consideration and calculations are crucial when deciding the most economical approach to handle balances.

For Instance, you have a $100 balance on a credit card with a 20% interest rate and aim to pay it off in one month.

The interest charges would be $1.67. Now, if you decide to go for a 3% balance transfer, which is a fee of $3, it would end up costing you more than just paying the interest.

How much balance can I transfer?

The amount allowed for balance transfer varies by credit card, with many cards allowing transfers up to the card’s credit limit, determined by your issuer and based on factors like your credit score.

However, some cards may impose specific restrictions on the transfer amount. To effectively utilize the balance transfer option, understanding these limitations is crucial.

How long does a balance transfer take?

Typically, balance transfers take 5 – 7 days to complete and appear in the account you’re transferring the balance to. Although, the duration can vary depending on the credit card issuer.

Some credit cards can take 14 or even 21 days to complete a balance transfer. It’s advisable to continue making payments on the old card to avoid any potential late fees or penalties during this time.

Types of Balances Transferable to a Credit Card

Credit cards generally accept balances from other credit cards, but not all allow transfers from loans or other non-credit card debts.

Understanding which types of balances are transferable is crucial when deciding whether to utilize a balance transfer option.

The table below outlines the credit card issuers and their corresponding credit cards’ flexibility in handling various types of debt.

It provides a comprehensive view of which credit cards allow balance transfers for different financial obligations, such as store cards, auto loans, student loans, HELOCs (Home Equity Lines of Credit), etc.

American Express leads the list with a broad range of transferable balances, followed by Chase and Citibank, offering flexibility in handling various debt categories.

| Credit Card Issuer | Credit Card | Store Card | Auto Loan | Student Loan | Mortgage | HELOC | Small Business Loan | Payday Loan |

|---|---|---|---|---|---|---|---|---|

American Express |

✔ |

✔ |

✔ |

✔ |

||||

Chase |

✔ |

✔ |

||||||

Citibank |

✔ |

✔ |

✔ |

✔ |

✔ |

✔ |

✔ |

✔ |

Bank of America |

✔ |

✔ |

✔ |

✔ |

✔ |

|||

Wells Fargo |

✔ |

✔ |

✔ |

✔ |

✔ |

✔ |

✔ |

|

Capital One |

✔ |

✔ |

✔ |

|||||

U.S. Bank |

✔ |

✔ |

✔ |

✔ |

||||

Discover |

✔ |

✔ |

✔ |

|||||

PenFed |

✔ |

✔ |

✔ |

✔ |

||||

Barclays |

✔ |

✔ |

||||||

USAA |

✔ |

Best Balance Transfer Credit Cards

The best balance transfer credit cards typically feature a 0% introductory balance transfer APR, $0 annual fees, and no low balance transfer fees of approximately 3%.

It’s essential to note that even the best balance transfer cards often come with a high regular APR.

A balance transfer calculator can help determine which card will yield the maximum savings in the long run.

Harnessing the power of a balance transfer credit card can be a valuable strategy in managing your debt effectively.

With a 0% APR offer, your payments can directly reduce the principal balance instead of being consumed by interest charges.

When selecting the right balance transfer card for your needs, consider the balance transfer fee, the amount of debt you intend to transfer, and the timeframe for repayment.

Best Credit Cards for Overall Balance Transfers

While managing credit card debt, finding the right balance transfer card can make a significant difference.

Here are two top contenders, each excelling in its own way, making them the best for overall balance transfers.

-

card_name

The card_name stands out for its impressive combination of an introductory APR of intro_apr_rate,intro_apr_duration, then reg_apr,reg_apr_type, no annual fee, and a rewarding cashback program.

This makes it an amazing choice for consolidating debt without compromising on additional perks. Terms Apply**.

-

card_name

For comprehensive balance transfers, the card_name offers a compelling intro_apr_rate,intro_apr_duration, as well as reg_apr,reg_apr_type and flexible

With no annual fee, this card provides great rewards, making it a top pick for individuals seeking a well-rounded solution to overseeing their credit card balances.

Best Credit Cards for Long Balance Transfers

Credit cards with extended balance transfer periods are invaluable for those focused on sustained debt reduction. Below are two perfect credit cards for long-balance transfers, each offering distinct advantages for prolonged financial stability.

-

card_name

The card_name takes the lead in catering to long-term balance transfers with its exceptional 0% introductory APR and no balance transfer fee.

It is a strategic choice for individuals seeking an extended period to pay their existing credit card balances without incurring additional charges.

-

Capital One Platinum Credit Card

The Capital One Platinum Credit Card comes with no balance transfer fees.

Its straightforward approach and favorable terms make it an ideal companion for those aiming for an extended timeframe to manage and reduce their credit card debt.

Best Credit Cards for Flat-Rate Cash Back

If you prefer simplicity and consistency in your credit card, then flat-rate cashback cards are the right fit for you! Here are the two best credit cards for flat-rate cash back, offering straightforward and rewarding experiences.

-

card_name

The card_name provides a hassle-free 1.5% cash back on every purchase.

Boasting simplicity and versatility, it gives cardholders a reliable way to earn rewards across all spending categories.

-

card_name

Another excellent card for flat-rate cashback is the card_name. It has an innovative structure: 1% cash back on purchases and an additional 1% cash back as you pay for those purchases.

This dual-reward system makes it an attractive choice for those seeking consistent rewards.

Best Credit Cards for Rotating Bonus Categories

For those who revel in the thrill of changing bonus categories, the credit cards for rotating bonus categories bring excitement and rewards. Explore 2 top bonus category credit cards known for their dynamic reward structures.

-

Chase Freedom Flex®

The Chase Freedom Flex® stands out as one of the best for rotating bonus categories, with its quarterly changing categories that align with everyday spending.

Cardholders can maximize their rewards with 5% cash back in diverse areas, such as groceries, streaming services, and dining

-

card_name

Renowned for its innovative approach, the card_name shines among the best, providing quarterly updates to its 5% cash back categories, which may include groceries, gas stations, or restaurants.

It caters to dynamic consumer preferences, providing an enticing credit card experience.

Best Credit Cards for Small Purchases

Some believe in the power of small purchases, as they bring forth tailored rewards and benefits. Delve into two exceptional options designed to amplify rewards for modest spending habits.

-

card_name

With a focus on everyday spending, the card_name is a top choice for small purchases.

It elevates your rewards game with generous cashbacks on essential categories like groceries, streaming services, and transit. Terms Apply**.

-

card_name

Crafted for flexibility, the card_name emerges as an excellent contender for small purchases.

Cardholders can choose their preferred 3% cash back category, including online shopping, dining, etc, offering tailored rewards that align seamlessly with personalized spending patterns.

Should you get a 0% Balance Transfer Card?

Opting for a 0% Balance Transfer Credit Card can be a savvy move, especially if you’re struggling with high-interest debt.

The introductory 0% APR period allows you to tackle the principal amount without accruing additional interest.

However, it’s crucial to weigh the pros and cons before making a decision.

Consider the balance transfer fee, the regular APR after the introductory period, and whether you can realistically pay off the debt within the promotional timeframe.

How much money can you save with a 0% balance transfer?

Utilizing a 0% balance transfer card can lead to substantial savings.

By avoiding interest during the promotional period, you can redirect funds toward paying down the principal debt, expediting your journey to financial freedom.

Assessing offers through a balance transfer calculator allows for a comprehensive evaluation of potential savings, factoring in transfer fees for informed decision-making.

Suppose you transfer a $5,000 balance from a card with a 20% APR to another credit card with a 0% APR offer for 12 months and maintain $500 monthly payments.

You could save $1,000 in interest payments alone, providing a significant financial advantage.

How to compare 0% balance transfer cards

To compare 0% balance transfer cards effectively, start by assessing your eligibility, as these cards typically require a credit score of 690 or higher, then focus on the following crucial factors.

-

Ensure that your existing debt is transferable to the desired card issuer, as most banks prohibit transfers between their cards.

-

Assess the length of the promotional period, as a more extended 0% APR duration provides more time for debt repayment. However, be mindful that extended periods may come with higher transfer fees.

-

Consider balance transfer fees, aiming for cards with lower or no fees. Compare these fees, typically ranging from 3% to 5%.

-

Evaluate post-promotional APR rates, ensuring they align with your financial plans.

-

Additionally, weigh rewards, annual fees, and benefits the issuers offer, enhancing the card’s long-term value.

Select a card without annual fees to optimize debt reduction.

Thoroughly comparing these aspects will guide you to the best 0% balance transfer credit card for your financial needs.

Alternatives to a 0% balance transfer

If a zero percent balance transfer isn’t the ideal solution for you, then you must explore alternative strategies to manage and reduce debt effectively.

While we understand that 0% balance transfer offers can be enticing, understanding alternative strategies is crucial for effective debt management.

The following suggestions provide insights into navigating financial challenges without solely relying on 0% balance transfers.

-

Pay more than the minimum due

Pay more than the minimum dueTo accelerate debt repayment, the key is to pay more than the minimum amount every month.

So, instead of sticking to minimum payments, allocate additional funds to expedite debt payoff. This proactive approach minimizes interest accumulation.

-

Find out your Eligibility for Lower Interest

Find out your Eligibility for Lower InterestContact your creditors to negotiate a lower interest rate, especially if your creditworthiness has improved.

It can significantly decrease the cost of carrying a balance and ease the financial burden, making debt more manageable and cost-effective.

-

Leverage a Credit Card Payoff Calculator

Leverage a Credit Card Payoff CalculatorUse online tools to create a customized debt repayment plan.

A credit card payoff calculator helps you visualize different scenarios, allowing you to make well-informed decisions for efficiently paying down balances.

-

Utilize Personal or Debt Consolidation Loans

Utilize Personal or Debt Consolidation LoansConsolidating debt through a personal or debt consolidation loan can simplify repayment.

These financial tools may offer lower interest rates and structured repayment plans, streamlining your path to debt-free living.

Best Balance Transfer Tips

Successfully managing a balance transfer requires thoughtful consideration, and the best tips can be invaluable in optimizing this financial strategy.

Whether aiming to consolidate debt, secure lower interest rates, or streamline payments, the right guidance makes all the difference.

Discover the best balance transfer tips that empower you to navigate your finances wisely without potential pitfalls and make the most of this powerful tool for debt management and financial stability.

-

Check your Credit Score

Regularly monitoring your credit score is crucial before initiating a balance transfer.

The best 0% balance transfer credit cards typically require good or excellent credit.

A higher score enhances your chances of approval and securing more favorable terms, ensuring a smooth transition.

Also, it’s advisable to check your credit score before applying to understand your eligibility.

-

Decide How Much to Transfer

Strategic planning is important when deciding the transfer amount.

Consider your repayment capacity and the promotional period, aiming for a balance that accelerates debt reduction without straining your budget.

Balance transfers don’t have to cover the full amount owed. Partial transfers are wise, allowing you to take advantage of a card’s 0% intro period without worrying about regular rates.

-

Check for Free Balance Transfer Offers

You can minimize costs by exploring credit cards with no transfer fees.

This ensures that every dollar you transfer goes towards reducing your debt, which maximizes your overall savings.

Some credit cards offer no balance transfer fees and a 0% balance transfer APR for a certain period, typically available to those with at least good credit.

Cards APR/Rates card_name intro APR of intro_apr_rate,intro_apr_duration, then reg_apr,reg_apr_type

card_name 0% intro APR for 18 months from account opening on purchases and balance transfers

Citi® Diamond Preferred® Card Intro APR of intro_apr_rate,intro_apr_duration, then reg_apr,reg_apr_type

-

Carefully Compare Offers

Make a thorough comparison of various balance transfer offers.

Assess introductory APR rates, fees, and post-introductory rates to make an informed decision that fulfills your financial goals and offers maximum savings.

-

Make a Payoff Plan

Strategically design your repayment strategy to align with the introductory APR period to ensure an efficient payoff.

A credit card payoff calculator can help plan monthly payments to become debt-free before regular rates kick in.

-

Understand the Various Ways to Leverage Balance Transfers

Beyond debt consolidation, explore innovative uses of balance transfers, such as refinancing high-interest loans or managing multiple debts for streamlined financial management.

Use them wisely, considering interest rates and potential savings.

-

Do Not Make New Purchases with your Balance Transfer Card

Maintain financial discipline by refraining from new purchases on your balance transfer card.

This focus ensures that all available funds contribute to debt reduction, preventing additional financial strain during the repayment period.

Use a separate rewards credit card for spending to maximize benefits.

FAQs

What is a balance transfer APR?

A balance transfer APR is the interest rate applied to the transferred balance on a credit card.

It is typically lower, often 0%, for a specified introductory period.

How long does a balance transfer take?

The duration of a balance transfer varies but usually takes 5 to 14 days, depending on the credit card issuer and the involved banks.

How do you qualify for zero interest balance transfer?

Qualifying for a zero-interest balance transfer usually requires a good to excellent credit score, typically around 690 or higher.

What does request held mean on balance transfer?

“Request held” on a balance transfer means the issuer is reviewing and processing your transfer, and it is temporarily on hold during this evaluation.

Can a balance transfer be denied?

Yes, a balance transfer can be denied based on factors like creditworthiness, available credit limit, or the bank’s policies.

Can you do a balance transfer with the same bank?

In most cases, you can’t transfer a balance within the same bank, such as moving a balance from one Chase card to another.

Can you do a partial balance transfer?

Some credit cards allow partial balance transfers, letting you transfer a portion of the total amount to the new credit card.

Can you transfer a balance multiple times?

While some cards may allow multiple balance transfers, there may be limitations, and it’s essential to check with the card issuer.

Can I still use my credit card after a balance transfer?

YES! You can still use your credit card after a balance transfer, but we recommend you avoid new purchases to focus on paying down the transferred balance.

How can I receive balance transfer offers?

To receive balance transfer offers, regularly check your mail, email, or the card issuer’s website.

Good credit and a history of on-time payments increase your chances of receiving such offers.

![Guide to Houston Intercontinental Airport Lounges: Top Things to Know [2025]](https://www.uthrive.club/wp-content/uploads/2024/11/Guide-to-Houston-Intercontinental-Airport-Lounges-Top-Things-To-Know-2024-1024x600.jpg)

![Guide to Seattle Airport Lounges: Top Things to Know [2025]](https://www.uthrive.club/wp-content/uploads/2024/11/Guide-to-Seattle-Airport-Lounges-Top-Things-To-Know-2024-1024x599.jpg)

![Guide to LaGuardia Airport Lounges: Top Things to Know [2025]](https://www.uthrive.club/wp-content/uploads/2024/10/Guide-to-Laguardia-Airport-Lounges-Top-Things-To-Know-2024-1024x600.jpg)

![Guide to SFO Airport Lounges – Top Things to Know [2025]](https://www.uthrive.club/wp-content/uploads/2024/10/Guide-to-SFO-Airport-Lounges-Top-Things-To-Know-2024-1024x599.jpg)

![Guide to Boston Airport Lounges: Top Things to Know [2025]](https://www.uthrive.club/wp-content/uploads/2024/10/Guide-to-Bostan-Airport-Lounges-Top-Things-To-Know-2024-1024x600.jpg)